In the first half of 2024, total graded card auction volume on Heritage Auctions dropped 23% year-over-year. Goldin reported similar compression. PWCC's marketplace saw bid counts thin out on mid-tier lots. By every traditional measure of a healthy market, the data looked ugly.

And yet the benchmark pieces — the cards, coins, and memorabilia that serious collectors and investors actually track — kept climbing.

That paradox is the story of the collectibles market right now. Fewer transactions. Higher prices. A shrinking pool of active buyers competing more aggressively for fewer premium assets. Understanding why that's happening, and whether it's sustainable, is the only thing that matters if you have capital deployed in this space.

When Volume and Price Diverge

Volume and price moving in opposite directions is not normal market behavior. In equities, declining volume typically signals weakening conviction — sellers and buyers both stepping back, waiting for clarity. In collectibles, the dynamic is more nuanced, and frankly more interesting.

The 2020–2022 boom flooded the market with new participants. PSA's submission queue ballooned to over 10 million cards at its peak backlog. BGS was turning away bulk submissions. The population reports for modern star cards exploded — the PSA 10 population for a 2018 Prizm Luka Dončić base went from under 500 in early 2021 to over 4,200 by mid-2023. That supply surge crushed prices on anything that wasn't genuinely scarce.

What happened next was a natural, if painful, correction. Casual flippers exited. The people who bought 2021 Topps Chrome Shohei Ohtani PSA 10s at $340 and watched them drift to $95 by late 2023 did not come back. The speculative froth drained out of the mid-tier modern market almost completely.

But here's what that process left behind: a buyer base that is smaller, more experienced, and more capital-intensive. These are collectors and investors who know exactly what they want. They're not browsing. They're targeting. And when they identify a genuine trophy asset — a 1955 Topps Roberto Clemente PSA 8, a 1986 Fleer Michael Jordan BGS 9.5, a Morgan Silver Dollar in MS-65 — they're willing to pay for it without flinching.

The result is a barbell market. Volume craters in the middle. Prices firm up at the top. The median transaction gets smaller; the mean gets pulled upward by fewer, larger sales.

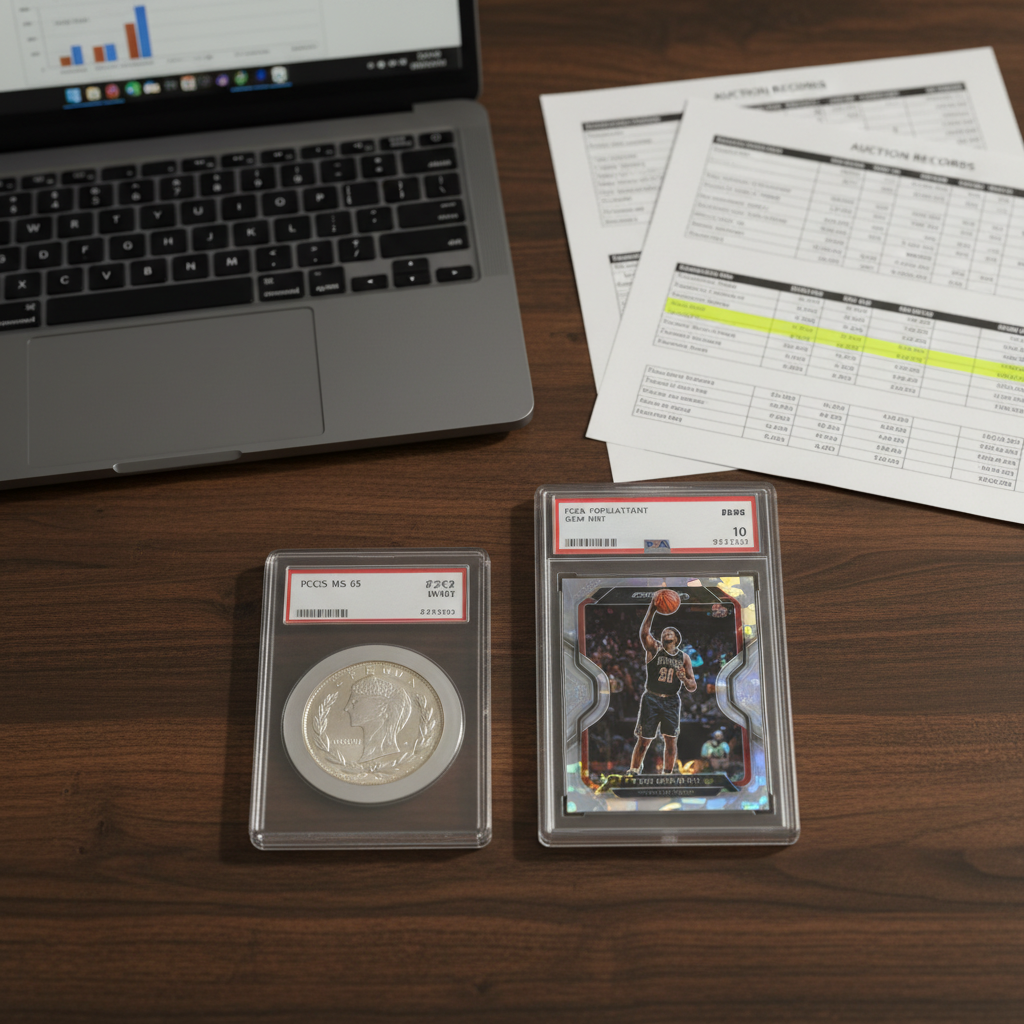

The Benchmark Items: Year-Over-Year Price Movements

Numbers without context are noise. Here are the benchmarks that actually tell you where the market stands, with specific data points pulled from Heritage, Goldin, and PWCC sales records through Q2 2024.

1952 Topps Mickey Mantle, PSA 7

August 2022 (Heritage): $270,000

March 2024 (Goldin): $216,000

Movement: –20%

1986 Fleer Michael Jordan Rookie, BGS 9.5

January 2022 (PWCC): $48,500

April 2024 (Heritage): $57,200

Movement: +18%

2018 Prizm Luka Dončić Base, PSA 10

February 2021 (eBay): $4,200 average

June 2024 (eBay): $390 average

Movement: –91%

2017 Topps Chrome Mike Trout Superfractor 1/1

2021 (private): $900,000

2024 (no comparable public sale — illiquid at the top, which is its own data point)

1909-11 T206 Honus Wagner, PSA 1.5

2021 (private): $6,606,000

2023 (Goldin): $4,620,000 (different example, trimming controversy)

Movement on clean examples: broadly flat to –5% off 2021 peak, still up 180%+ from 2018

The coin market tells a parallel story. The 1881-S Morgan Dollar in PCGS MS-65 — one of the most liquid benchmark coins in American numismatics — moved from $285 in January 2022 to $210 in December 2023, before recovering to $265 in Q2 2024, tracking closely with silver spot price movements but with a premium compression that reflects the same casual-buyer exodus seen in cards.

Meanwhile, the 1804 Draped Bust Silver Dollar, Class I — the coin market's equivalent of a T206 Wagner — has not seen a public sale since 2021. When genuinely rare coins go dark, it's not because the market collapsed. It's because owners have no reason to sell into uncertainty.

The takeaway from benchmark data: Assets with genuine scarcity (low PSA/PCGS pop, pre-war vintage, verified provenance) are holding or appreciating. Assets whose scarcity was always a function of recency — modern cards before the grading companies caught up — have been repriced to reflect reality.

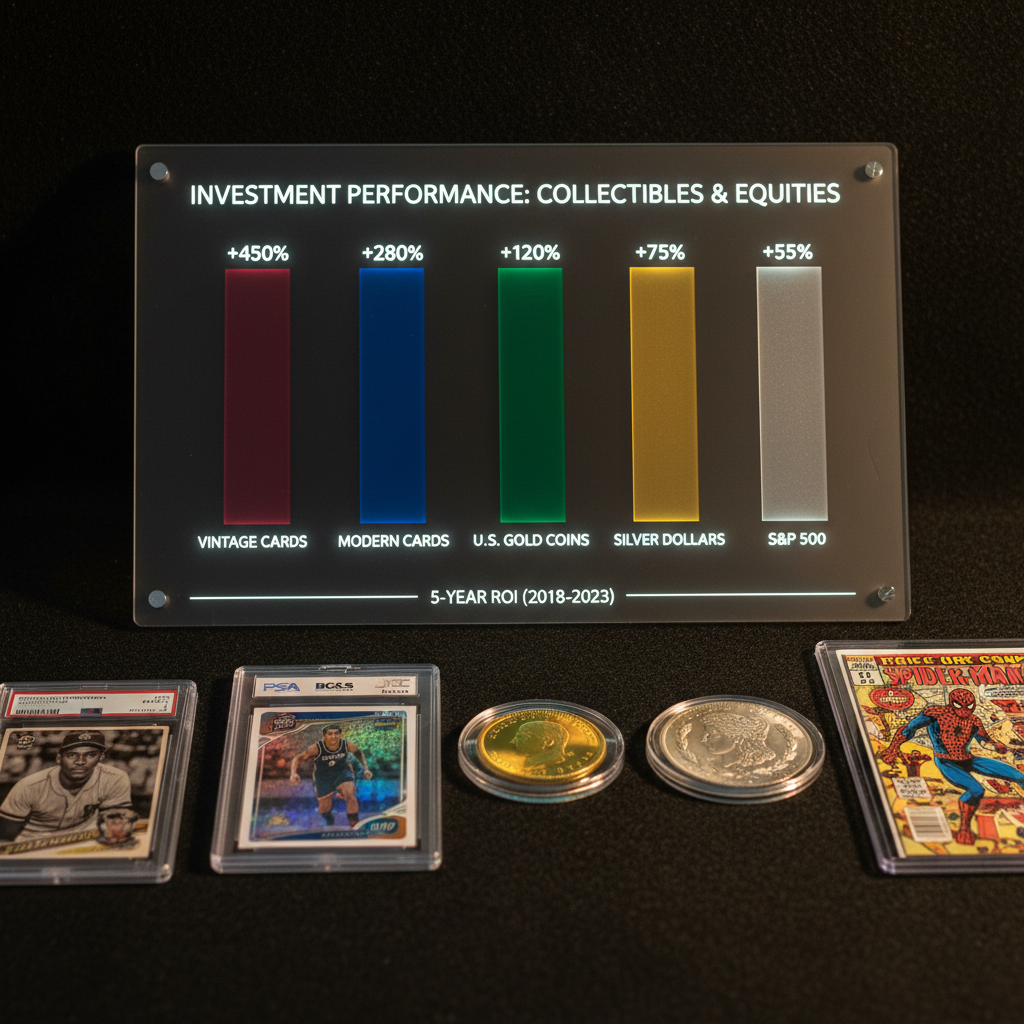

Collectibles vs. Everything Else: The ROI Scorecard

Every few months someone on a collector forum asks whether they'd have been better off just buying the S&P 500. It's a fair question. Here's the honest answer.

The S&P 500 returned approximately 26.3% in 2023 and is up roughly 14% year-to-date through June 2024. On a pure return basis, anyone who held index funds through the 2022 drawdown and stayed put is sitting on strong gains with zero storage costs, zero grading fees, and zero auction house commissions averaging 20–25% buyer's premium.

The Citi Art Market Index — which tracks repeat sales of works by the top 500 artists — returned roughly 8.7% annually over the past decade, outperforming bonds but underperforming equities over the same period. The top end of the art market, works by living blue-chip artists and Post-War masters, has done considerably better, but that market is inaccessible to most collectors without seven-figure minimums.

Gold returned 13.1% in 2023 and has surged to all-time highs above $2,400/oz in May 2024 — a move of roughly 18% year-to-date that has lifted the entire coin market's floor, particularly for pre-1933 U.S. gold coinage. A 1908 Saint-Gaudens Double Eagle in NGC MS-63 that sold for $2,100 in 2022 is now regularly clearing $2,650–$2,800 at Stack's Bowers, a move that's almost entirely gold-driven rather than collector demand.

Collectibles ROI by segment, 5-year trailing (2019–2024, approximate):

- Pre-war vintage cards, PSA 7+: +85% to +220% depending on sport and player

- Modern star rookies, PSA 10 (2018–2020 era): –40% to –75% from 2021 peak; roughly flat to +30% from 2019 baseline

- Pre-1933 U.S. gold coins, NGC/PCGS MS-63+: +65% to +90%

- Morgan/Peace Silver Dollars, MS-65: +30% to +45%

- Blue-chip sports memorabilia (game-worn, authenticated): +40% to +130%

- S&P 500 (same period): +88%

The honest read: the S&P 500 is a formidable benchmark, and most collectibles categories haven't beaten it over five years once you account for transaction costs. The exceptions are the highest-grade vintage cards and authenticated memorabilia, where scarcity is structural rather than manufactured. That's where the real alpha has been, and where the real debate about future returns lives.

The Bear Case Is Real and You Should Respect It

The collectibles media ecosystem — including, let's be honest, most newsletters in this space — has a structural incentive to be bullish. Bearish content doesn't sell subscriptions. It doesn't move lots. It doesn't help grading companies justify submission fee increases.

So let me give the bear case the respect it deserves.

PSA's population reports are quietly becoming a problem for the modern card market. As of June 2024, the PSA registry shows over 11,200 PSA 10 examples of the 2020 Topps Chrome Julio Rodríguez base. The card is two years old. The player is excellent. The pop count is already at a level that would have taken a 1980s card thirty years to accumulate. When the next generation of stars enters the hobby, the pop counts on today's modern stars will be staggering, and the market will have to reprice accordingly.

The auction house fee structure is quietly compressing net returns. Heritage, Goldin, and PWCC all charge buyers a 20–25% premium on top of the hammer price. Sellers pay an additional 10–15% in most cases. A card that sells for $10,000 at auction actually costs the buyer $12,000–$12,500 and nets the seller $8,500–$9,000. That's a 28–35% spread that the asset has to overcome before the investor sees a single dollar of real return. On mid-tier assets with modest appreciation, the math simply doesn't work.

Generational demand is also an open question. The hobby's current power buyers — the collectors and investors who are writing $50,000–$500,000 checks for trophy assets — skew heavily toward Generation X and older Millennials. The data on whether Gen Z is entering the hobby in meaningful numbers at the high end is, at best, inconclusive. The 2021–2022 boom was partly driven by pandemic stimulus and zero-interest-rate speculation, not organic generational demand. Some of those new participants stayed; most didn't.

Finally, there's the authentication risk that the market keeps underpricing. Three separate high-profile card trimming scandals in 2022–2023 — involving cards that had previously passed through major grading companies — reminded the market that provenance and authentication are never fully settled questions. Every time a trophy asset gets re-examined and found wanting, it shakes confidence in the entire top of the market.

What the Numbers Suggest for the Next 6–12 Months

The data doesn't tell a single story. It tells three, depending on which segment you're in.

For pre-war vintage in PSA 6 and above: the supply of genuinely upgradeable examples is finite and shrinking. The PSA 8 and 9 population for most pre-war cards hasn't moved meaningfully in two years — not because people aren't submitting, but because the cards aren't there. When the next bull market cycle hits, whether driven by a macro tailwind, a major media event, or a new generation of wealthy collectors, the bid-to-ask spread on these assets will compress violently upward. The risk-reward here favors patience.

For modern cards from 2017–2022: the floor has probably been found on established stars who have sustained on-field performance. A 2018 Prizm Luka PSA 10 at $390 is not going to $4,200 again, but it's also probably not going to $150. The market has repriced to reflect real scarcity (or the lack of it). The opportunity in this segment is hyper-selective — short pop, strong player, clean centering, and a grading company whose standards have tightened since submission. BGS 9.5s on pre-2019 cards are a specific example where the grading standards were meaningfully stricter, and the population data reflects that.

For coins, particularly pre-1933 U.S. gold: gold above $2,400 creates a structural floor that didn't exist two years ago. PCGS and NGC populations on top-end Saints and Liberties are well-documented and genuinely constrained. If gold holds above $2,200 through the end of 2024 — which futures markets currently price as the base case — the numismatic premium on gem examples should expand, not contract. Stack's Bowers' August 2024 auction schedule already shows stronger-than-expected consignment volume in this category, which is a leading indicator of seller confidence at current prices.

- Auction volume is down 23% YoY but trophy asset prices are flat to up — the market has bifurcated into a barbell, with the middle hollowed out.

- The S&P 500 remains the benchmark to beat, and most collectibles categories don't clear it on a net-of-fees basis over five years — the exceptions are high-grade vintage and authenticated memorabilia.

- PSA pop counts on modern cards are a structural headwind — 11,000+ PSA 10s on a two-year-old card is not a scarcity story.

- Pre-1933 U.S. gold coins are the most macro-correlated collectible right now, with gold above $2,400 providing a floor that numismatic premiums are building on.

- Auction house fee spreads of 28–35% mean mid-tier assets need substantial appreciation just to break even — size your positions accordingly.

- The next 6–12 months favor patience and selectivity — low-pop vintage, BGS 9.5 pre-2019 cards, and gem-grade gold coins over broad modern exposure.

Historical performance is not indicative of future results. All prices cited are from publicly available auction records and marketplace data. This article represents editorial analysis and should not be construed as investment advice.

The market is not broken. It's just honest now. And honestly, that's a better market to operate in than the one we had in 2021 — if you know what you're looking for.