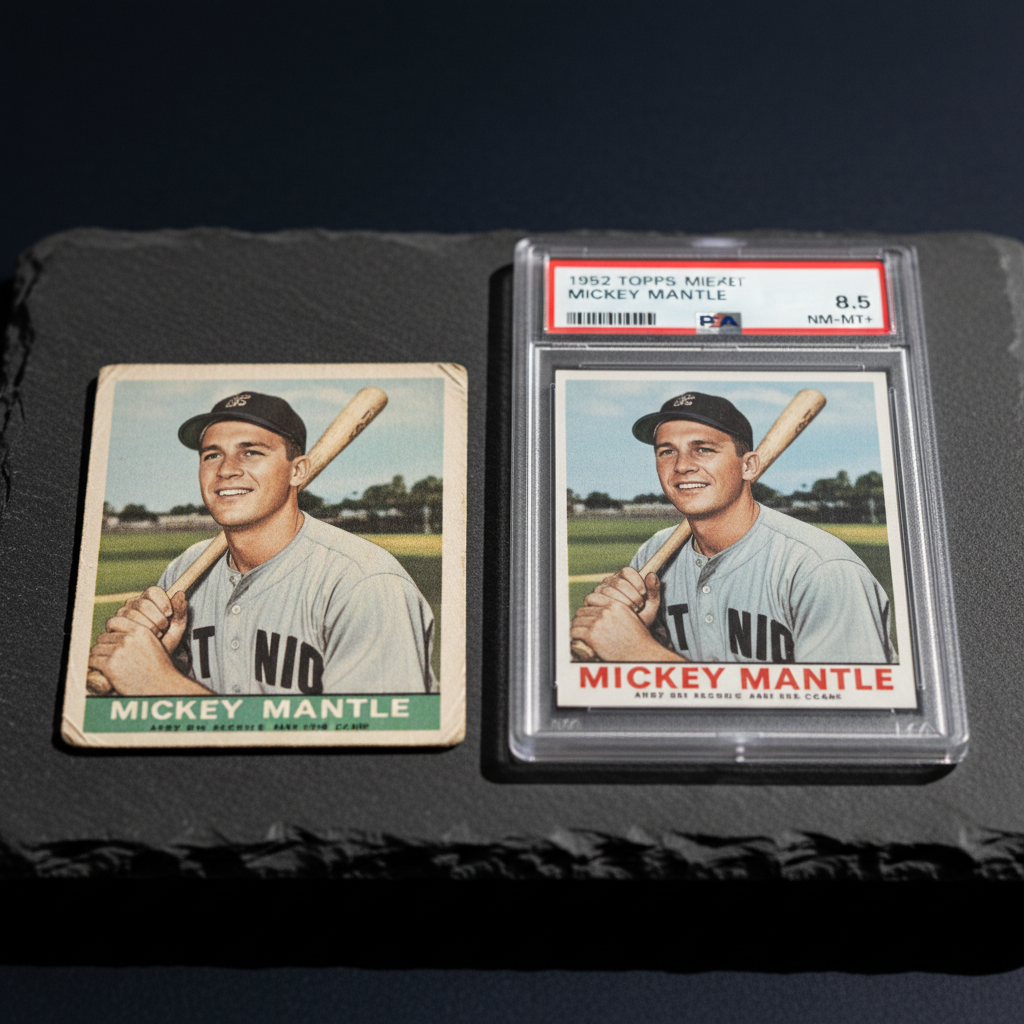

In Heritage Auctions' February 2024 catalog, a raw 1952 Topps Mickey Mantle graded Excellent by the seller's generous eye sold for $41,000. Six months later, a nearly identical example — same centering, same surface wear, same corner rounding — crossed the block at Goldin for $28,500. No explanation. No scandal. No flood of supply. The market simply repriced the uncertainty.

That gap — $12,500 in six months on a single ungraded card — tells you everything you need to know about where raw vintage baseball cards are heading, and why the collectors still chasing them without third-party authentication are playing a game that the market has quietly decided to stop rewarding.

The Authentication Premium Is No Longer Optional

Let's establish the baseline first. The vintage baseball card market — defined here as cards issued before 1980, anchored by the T206, 1933 Goudey, and 1952 Topps sets — has historically operated on two parallel tracks. Dealers, LCS shops, and old-school collectors traded raw cards by eye. The grading market ran alongside it, adding a premium for slabbed examples but never quite killing the appetite for unencapsulated cardboard.

That coexistence is fracturing. And the fracture line runs directly through buyer confidence.

PSA's authentication volume tells the story bluntly. In 2019, PSA processed roughly 6.8 million total submissions. By 2023, that number had surged past 14 million annually, even accounting for the service backlog chaos of 2021. A meaningful portion of that growth came from vintage submitters — collectors and dealers who previously held raw inventory and are now converting it to slabs in anticipation of a market that increasingly demands the paper trail.

The premium gap between graded and raw has widened to the point where it reshapes transaction logic. A PSA 4 (VG-EX) 1952 Topps Willie Mays — not a glamorous grade, not a registry card — has consistently cleared $8,000 to $11,000 at Heritage and Stack's Bowers over the past 18 months. Comparable raw examples with honest condition descriptions have struggled to break $5,500 on the same platforms. That's not a small spread. That's a structural repricing of risk.

The authentication premium on mid-grade vintage has expanded from roughly 20% to 60-80% over five years. That's not hype — it's the market pricing in the cost of uncertainty.

Why does a PSA 4 command that kind of premium over an honest raw VG-EX? Because PSA 4 means something specific. It means no alterations, no recoloring, no trimming. It means the card's dimensions have been verified. It means a second buyer — whether that's a collector in Tokyo or a fund manager in Connecticut — can price the card without flying to examine it. Liquidity has a value. In a market that has gone genuinely global, that value has become enormous.

Why the Repricing Is Happening Now, Not Five Years Ago

The timing isn't accidental. Three forces converged between 2020 and 2024 to accelerate what had been a gradual drift into a decisive market shift.

First: the fraud exposure cycle. The 2020-2021 card boom brought an enormous influx of new buyers who had never held a T206 Honus Wagner and didn't know what a trimmed corner felt like. Predictably, fraud spiked. Heritage Auctions and PWCC both tightened their raw lot vetting procedures after several high-profile disputes over altered vintage cards. PWCC's marketplace, which processes tens of thousands of vintage transactions monthly, began flagging raw vintage listings with condition disclaimers that would have seemed excessive five years earlier. The message to buyers was unmistakable: proceed with caution.

When major platforms signal caution, sophisticated buyers listen. And when sophisticated buyers exit a tier of the market, prices follow them out the door.

Second: the rise of institutional and semi-institutional money. The collectibles asset class attracted serious capital during the pandemic era — family offices, fractional ownership platforms like Collectable and Rally, and high-net-worth individuals who treat cards as portfolio diversification rather than childhood nostalgia. Institutional buyers don't buy raw. Full stop. They require encapsulated, authenticated, population-verified assets that can be priced against comparable sales with confidence. As this buyer class grew from a curiosity to a meaningful market force, it pulled auction house strategy with it. Heritage now dedicates separate catalog sections to graded vintage. Goldin's top-tier lots are almost universally slabbed. The catalogs themselves have become editorials on what the market values.

Third: SGC's resurgence changed the competitive dynamic. For most of the 2010s, PSA was the dominant choice for vintage grading with SGC as a distant second. The pandemic era reshuffled that hierarchy. SGC's faster turnaround times, cleaner slab design, and — critically — its reputation for tighter grading standards on vintage material attracted a wave of serious collectors who felt PSA's vintage grades had grown inconsistent. By 2022, SGC-graded T206 and early Goudey cards were routinely trading at or above PSA equivalents on eBay and at Stack's Bowers, a reversal that would have seemed implausible in 2018. When two credible grading options exist, the raw alternative looks even less attractive. Why accept uncertainty when you have two strong certified paths?

These three forces didn't create the authentication premium from scratch. But they compressed a decade of gradual change into four years, and the raw market absorbed that compression as a price correction it wasn't prepared for.

The Grade Gap: What PSA and SGC Population Reports Actually Tell Us

Population reports are the market's X-ray machine. If you're not reading them before buying vintage, you're navigating blind.

Consider the 1933 Goudey #53 Babe Ruth — the portrait card, the one with the clean red background. PSA's population report as of early 2024 shows 847 graded examples across all grades, with just 14 graded PSA 7 (NM) or above. That top-grade scarcity is the reason a PSA 7 example sold for $312,000 at Goldin in November 2023. But the more instructive number is the PSA 4 and PSA 5 population: combined, roughly 290 examples. Those are the mid-grade cards most collectors can actually afford, and they're the tier where the raw-versus-graded price gap is most pronounced and most consequential for typical buyers.

A raw 1933 Goudey Ruth in honest VG condition has sold in the $18,000 to $24,000 range at various Heritage catalog sales over the past two years. A PSA 3.5 (VG+) example cleared $34,500 at Stack's Bowers in January 2024. The PSA 3.5 isn't a better-looking card in any aesthetic sense — a VG+ Goudey Ruth is a VG+ Goudey Ruth. But it's a verified, authenticated, market-liquid asset. The buyer who paid $34,500 knows exactly what they own. The buyer who paid $22,000 for the raw copy knows they own a card that looks like an authentic 1933 Goudey Ruth.

That distinction, once philosophical, is now financial.

SGC's population data reinforces the same conclusion from a different angle. SGC has graded significantly fewer vintage cards than PSA historically, which means SGC-population cards often carry a scarcity premium on top of the authentication premium. A T206 Ty Cobb (red portrait background) graded SGC 4.5 sold for $58,000 at Heritage in March 2024, against a PSA 4 comp from the same period at $49,000. The SGC premium on that specific card was roughly 18% — explainable partly by lower population, partly by SGC's reputation for conservative vintage grading. Collectors who understand this dynamic can exploit grade-company arbitrage. Collectors who don't, and who are buying raw to avoid the grading cost, are leaving money on the table in both directions: paying less for raw cards, yes, but also receiving significantly less when it's time to sell.

The population data also reveals something the raw market can't see: the upgrade ceiling. Before submitting a raw vintage card, experienced collectors cross-reference the population report to determine whether the card's apparent condition has a realistic shot at a grade that will clear the authentication premium threshold. A card that looks like a PSA 5 but sits in a population where PSA 5 is the most common grade has limited upside. A card that looks like a PSA 5 but where only eight PSA 5s exist is a different proposition entirely. Raw buyers are making that calculation blind.

The Contrarian Case for Raw Cards — and Why It's Mostly Wrong

The bear case for this thesis deserves honest treatment, because it's not entirely without merit.

The most coherent argument for raw vintage is the grading cost and turnaround risk. PSA's current pricing tiers for vintage cards — cards issued before 1980 — start at $150 per card at the Economy level and climb to $600+ at the Express level, with declared value caps that limit submission options for high-value raw cards. If you're buying a raw VG-condition 1955 Topps Sandy Koufax rookie for $800 and the grading fee is $150 with a 60-day turnaround, the economics are tighter than they look. You're paying 19% of purchase price for authentication, with no guarantee the grade comes back at a number that justifies the spread.

There's also the aesthetics argument, which serious old-school collectors make with more passion than the market probably warrants. A raw card has texture — the ability to hold it, feel the cardboard, examine the surface under a loupe. Slabbing removes that intimacy and locks the card in plastic that, if damaged, requires cracking and resubmission. Some collectors, particularly those who have been in the hobby for decades, view the slab as a product of financial speculation rather than genuine appreciation. They're not entirely wrong about the cultural shift. They're just wrong about where the market is going.

The strongest version of the contrarian argument is the set-completion strategy. Collectors building complete T206 sets — all 524 subjects, including the minor league variations — cannot realistically afford to grade every card. A complete T206 set contains hundreds of common players worth $50 to $300 in mid-grade. Grading fees would exceed card values on a significant portion of the set. For set completionists, raw cards remain the only economically rational path. This is a real and legitimate use case.

But here's why the contrarian case is mostly wrong rather than entirely wrong: the set-completion argument applies to the long tail of vintage commons, not to the key cards that drive portfolio value. Nobody is arguing that you need to slab every 1933 Goudey common or every T206 minor leaguer. The authentication premium is concentrated in the cards that matter — Hall of Famers, rookies, short prints, and condition rarities. Those are precisely the cards where raw buyers are getting punished most severely by the current market. If your vintage strategy involves buying key cards raw to save on grading costs, you're optimizing for the wrong variable.

The vintage dealers who are thriving right now are the ones who figured this out earliest. They buy raw, grade aggressively, and sell slabbed. They're not collectors — they're operators. And the spread between what they pay for raw and what they receive for graded is the market's clearest signal about where value actually lives.

Where This Market Goes From Here

The authentication premium on vintage baseball cards will continue to widen over the next three to five years. That's not a guess — it's the logical endpoint of the forces already in motion.

Institutional capital doesn't leave collectible markets once it enters; it deepens its position and raises the infrastructure standards for everyone else. As long as family offices and fractional platforms are buying vintage baseball cards — and they are, with no visible sign of retreat — the demand for authenticated, liquid, population-verified assets will outpace the supply of newly graded material. PSA's submission volume has been growing, but vintage supply is fixed. You can't manufacture more 1952 Topps Mantles. Every card that gets slabbed permanently reduces the raw supply and, perversely, makes the remaining raw cards harder to sell.

The grading company landscape itself will likely consolidate or stratify over the same period. PSA remains the dominant brand for resale liquidity — a PSA-graded vintage card will always find a ready buyer. SGC has carved out a genuine premium niche for pre-war material. BGS (Beckett Grading Services), which built its reputation on modern cards with its subgrade system, has less of a foothold in the vintage space and faces an uphill battle to change that perception. Collectors buying vintage with a resale horizon should be submitting to PSA or SGC — the choice between them depends on the specific card, the population dynamics, and the target buyer — and should be treating the grading fee as a transaction cost, not an optional upgrade.

The raw vintage market won't disappear. Set completionists, dealers who flip quickly, and collectors who simply prefer unencapsulated cards will maintain a floor. But the ceiling — the aspirational price, the record sale, the number that gets written about — will belong exclusively to graded examples for the foreseeable future.

One more thing worth saying directly: the collectors who feel nostalgic about the raw market, who remember when a handshake and a dealer's reputation were authentication enough, aren't wrong to feel that something has been lost. The hobby has professionalized in ways that are financially rational and culturally flattening simultaneously. But nostalgia doesn't pay the spread. The market has made its decision about what it values, and it values certainty.

The raw vintage card is becoming an artifact of how the hobby used to work. The graded vintage card is how it works now.

- The authentication premium on mid-grade vintage baseball cards has expanded from roughly 20% to 60-80% over five years, representing a structural repricing of uncertainty rather than a temporary trend.

- PSA and SGC population reports are essential tools for understanding grade scarcity and upgrade ceilings — buying raw without cross-referencing population data is navigating blind.

- Three forces drove the repricing: fraud exposure in the 2020-2021 boom, the rise of institutional buyers who require authenticated assets, and SGC's resurgence as a credible second grading standard for vintage material.

- The contrarian case for raw cards is legitimate only for set-completion strategies on commons — for key cards (Hall of Famers, rookies, condition rarities), raw buyers are consistently leaving significant money on the table.

- SGC-graded pre-war material has achieved parity with or premium over PSA equivalents on specific vintage sets, creating grade-company arbitrage opportunities for sophisticated buyers.

- The authentication premium will continue widening as institutional capital deepens its position in the vintage market and fixed supply of authentic cards shrinks relative to grading demand.